Quick support from trusted insurance professionals Call +1 713-777-2886 today!

Quick professional support Call +1 713-777-2886 today!

Quick professional support Call +1 713-777-2886 today!

Table of Content

Title

Let AZ Insurance Help You

Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto Insurance Help You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

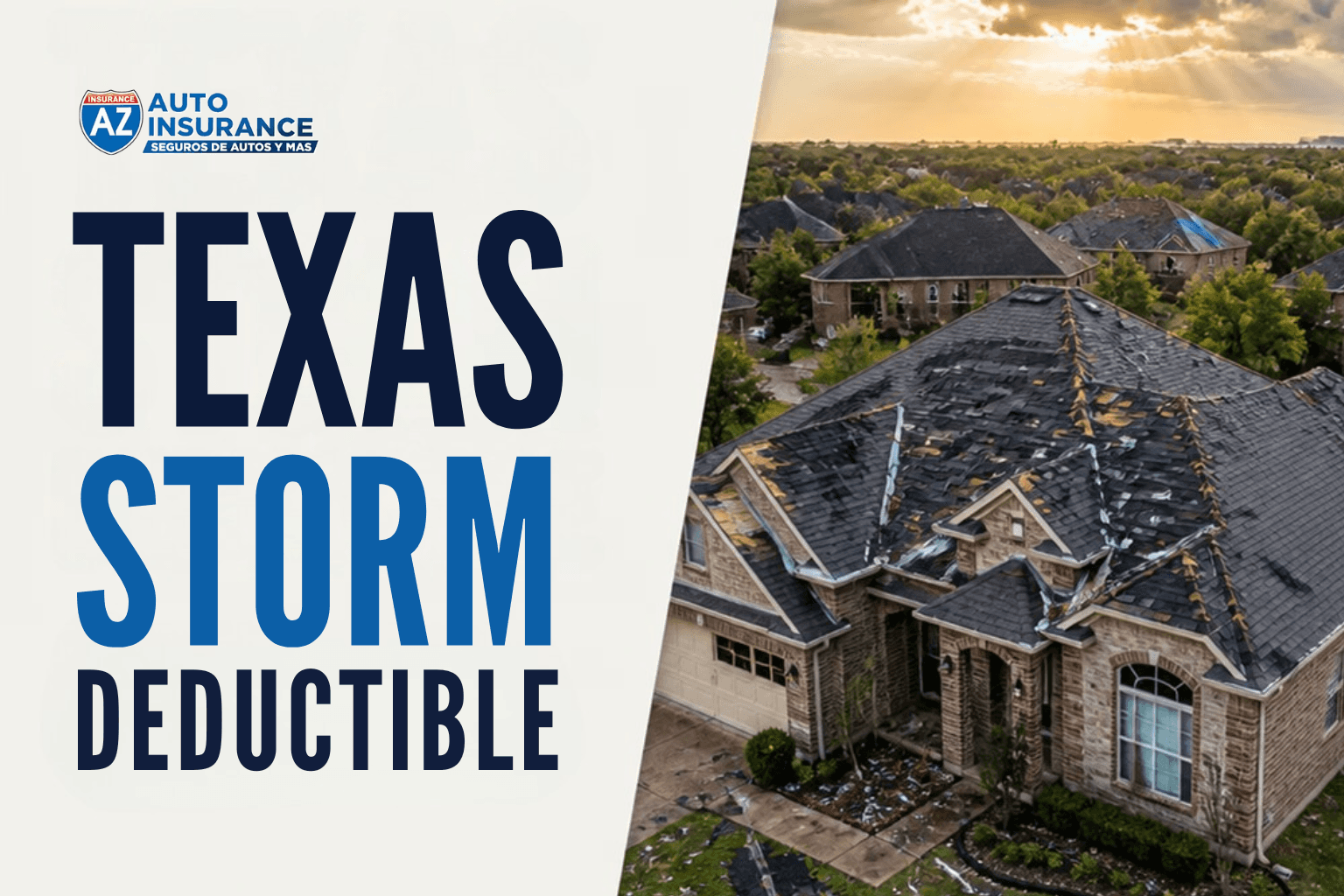

Texas Storm Deductible Explained: Why 2% Doesnt Mean $200 (And What To Do About It)

Texas Storm Deductible Explained: Why 2% Doesnt Mean $200 (And What To Do About It)

Texas Storm Deductible Explained: Why 2% Doesnt Mean $200 (And What To Do About It)

Texas Storm Deductible Explained: Why 2% Doesnt Mean $200 (And What To Do About It)

Texas Storm Deductible Explained: Why 2% Doesnt Mean $200 (And What To Do About It)

Reviewed by AZ Insurance Agency, licensed in Texas, serving Houston since 2003. AZ Insurance compares 8 carriers per quote across Houston, Sugar Land, Katy, and the greater metro area.

The storm came through on a Tuesday afternoon. By Thursday morning the adjuster was standing in the driveway, photographing the roof and the fence and the side of the house where the siding had peeled back. By the following Monday there was a claims summary in the inbox: covered damage totaling $9,400. And then, a number no one had prepared for.

The deductible: $7,800.

Not the $1,000 the homeowner remembered from when they signed the policy. Not the $500 they vaguely recalled discussing at the kitchen table years ago. $7,800 — because the home was insured for $390,000 and the wind/hail deductible on the policy was 2 percent of the insured dwelling value.

Two percent sounds almost harmless. Two percent sounds like rounding error. Two percent on a Texas home is not $200. In most cases it is not even close.

This is the most expensive misunderstanding in homeowners insurance in Texas today. And it is almost always discovered at the exact moment it does the most damage: after a storm, when the claim is already in motion and there is nothing left to negotiate.

What Most Texas Homeowners Believe About Their Deductible

Ask a homeowner in the Houston suburbs what their deductible is and most of them will give you a flat number. $1,000. $2,500. Maybe $500 if they bought the policy when rates were lower. That flat number is what they remember from the application, from the agent conversation, from the disclosure they signed three or four years ago and have not thought about since.

That flat number is real. It appears on the policy. It applies to most claims.

But it does not apply to wind or hail.

In Texas, homeowners insurance policies routinely carry a second deductible — a separate, higher deductible that applies specifically when the damage is caused by wind, hail, or a named storm. This second deductible is expressed as a percentage of the home's insured value, not as a flat dollar amount.

Here is what that looks like in practice:

$300,000 insured home with a 2% wind/hail deductible: $6,000 out of pocket before the carrier pays anything

$350,000 insured home with a 2% wind/hail deductible: $7,000 out of pocket

$400,000 insured home with a 2% wind/hail deductible: $8,000 out of pocket

$450,000 insured home with a 2% wind/hail deductible: $9,000 out of pocket

$500,000 insured home with a 2% wind/hail deductible: $10,000 out of pocket

Suburban Houston, Sugar Land, and Katy are densely concentrated with homes in exactly this price range. A 2% deductible at these values is not a minor cost-sharing mechanism. It is a five-figure gap between what the policy covers and what lands in the homeowner's hands.

And in Texas, storm season is not an abstract risk. It is a recurring annual event.

Why Texas Policies Work This Way

Texas sits in one of the most active storm corridors in the country. The state absorbs more hurricane activity than any other continental state, and the interior corridor — including the entire greater Houston metro — sees severe thunderstorm and hail events that routinely cost insurers hundreds of millions of dollars in a single season.

Carriers responded to this exposure years ago by restructuring deductibles. Instead of absorbing the first $1,000 of every wind and hail claim, they began shifting more of the initial loss to homeowners through percentage-based deductibles. This allowed them to continue offering coverage in Texas at all — without it, many carriers would have simply exited the state, which some have done anyway.

What this means for homeowners:

The flat deductible (also called the All Other Perils or AOP deductible) still applies to water damage, theft, fire, and most non-wind events

The wind/hail deductible (also called the Named Storm Deductible on some policies) applies whenever wind or hail is the primary cause of loss

Both deductibles appear in the same policy — one document, two separate deductible structures, and most people only ever notice the first one

The Texas Insurance Code requires carriers to disclose percentage deductibles clearly in the policy documents. The law is on the homeowner's side. The problem is not disclosure — the problem is that most homeowners do not read their Declarations Page until they have a reason to, and by then it is often after a loss.

Where To Find Your Wind/Hail Deductible Right Now

You do not need to wait for a storm to find out what your exposure is. The information is already in your policy.

Pull out your homeowners insurance Declarations Page — it is the one-to-two-page summary that comes at the beginning of your policy document. It is also available through your carrier's online portal if you have one. Once you have it, look for any of these labels:

Wind/Hail Deductible

Named Storm Deductible

Hurricane Deductible

Windstorm Deductible

Wind Percentage Deductible

The value next to that label will be expressed either as a percentage (1%, 2%, 3%) or, if you have a carrier that offers it, as a flat dollar amount. If it is a percentage, multiply it by your dwelling coverage amount — the Coverage A figure on the same page — and that is your out-of-pocket exposure for any wind or hail claim.

A few things to check while you have the page open:

Is your Coverage A amount current? If you bought your home several years ago and have not updated your dwelling coverage, your insured value may be below what it would cost to rebuild the home today. That affects your deductible math and your claim payout

Is the deductible 1%, 2%, or higher? Some Texas policies carry 3% or even 5% wind/hail deductibles, particularly in coastal and near-coastal areas

Is there a separate hurricane deductible? Some policies split wind/hail and hurricane into two separate percentage deductibles

What is the effective trigger? Some named storm deductibles only activate when a storm is officially named by the National Hurricane Center — an important distinction for inland hail events

If anything on that page is unclear, that is exactly what an independent agent is for. At AZ Insurance, a coverage review costs nothing and takes about twenty minutes.

The Moment Most Homeowners Find Out — and Why It Is Too Late

Here is the pattern AZ Insurance sees repeatedly.

A storm moves through the Houston area in spring or early summer. Hail hits the northwest suburbs. Damage is widespread. The homeowner files a claim. The adjuster comes out, documents the roof damage, the gutters, potentially the siding, and produces a damage estimate. Let's say that estimate comes in at $9,000.

The homeowner is relieved. Nine thousand dollars covers a new roof. They start calling roofers.

Then the Explanation of Benefits arrives. The carrier has applied the wind/hail deductible. The home is insured for $450,000. The deductible is 2%. That is $9,000. The claim payout: $0. Or close to it. The carrier owes nothing until the damage exceeds the deductible — and in this case they are exactly equal.

The homeowner now owes the full cost of the roof repair out of pocket, with no reimbursement, on a policy they have paid premiums on for years.

This is not fraud. This is not the carrier acting in bad faith. This is a contractual structure the homeowner agreed to and, in most cases, never fully understood. The Texas Insurance Code required disclosure. The disclosure happened. The homeowner signed and moved on.

The remedy is not outrage after the claim. The remedy is reading the policy before the storm.

Can You Get a Flat-Dollar Wind/Hail Deductible in Texas?

Yes — but it comes at a cost, and availability depends heavily on which carrier you are with and where your home is located.

Some Texas homeowners insurers offer flat-dollar wind/hail deductible options. Instead of 2% of the insured value, the policy might offer a $5,000 or $10,000 flat deductible for wind and hail. In some cases you can buy the deductible down to $2,500 with an endorsement.

The tradeoff is premium. Flat-dollar wind deductibles transfer more of the initial loss back to the carrier. Carriers price that risk into the annual premium. Depending on your home value, risk profile, and the carrier, a flat-dollar wind deductible might cost you an additional $200 to $600 per year.

Whether that is worth it depends on the math:

On a $400,000 home with a 2% deductible: your wind/hail exposure is $8,000. If you can cap that at $5,000 flat for an extra $300/year, you are buying down $3,000 of risk for $300. That is a 10-to-1 leverage ratio. Most financial planners would call that a good trade

On a $250,000 home with a 2% deductible: your wind/hail exposure is $5,000. Paying $400/year extra to bring that to $2,500 flat means you need to file a wind claim within 6 years to break even. Depending on your neighborhood's storm history, that may or may not pencil

The calculation is different for every household. It depends on the home's value, the premium differential available in the market, the carrier options in your area, and how much liquidity you have if a major storm claim comes in.

This is exactly the kind of comparison that shopping across multiple carriers makes possible. The flat-dollar option your current carrier does not offer might be available through a different one — at a premium you can absorb.

What the Texas Department of Insurance Says About These Deductibles

The Texas Department of Insurance (TDI) regulates homeowners insurance in Texas and has issued clear guidance on wind and hail deductibles. Per TDI:

Carriers are required to clearly disclose wind/hail and named storm deductibles in the policy documents before the policy is issued

The Declarations Page must prominently list the deductible amount and the method by which it is calculated (percentage of Coverage A is the most common)

Carriers cannot add a wind/hail deductible mid-term without providing advance written notice and the right to cancel

Homeowners have the right to request a plain-language explanation of how any percentage deductible will be calculated in the event of a claim

The TDI Consumer Guide to Homeowners Insurance (tdi.texas.gov/consumer/homeins.html) and the dedicated windstorm insurance page (tdi.texas.gov/consumer/windstorm.html) both contain information homeowners can reference when reviewing their policies or disputing a claim decision.

A few things TDI cannot do:

TDI cannot force a carrier to lower your deductible. The deductible is a contractual term. If you want different terms, you need a different policy or a different carrier

TDI cannot reverse a valid claim decision. If the damage falls below your deductible, the carrier owes nothing — this is not a claims handling error, it is the policy working as written

TDI cannot shop the market for you. That is what an independent agent does

Knowing your rights under Texas Insurance Code is useful. It will not replace the knowledge gap between what your current policy says and what better options look like on the open market.

Why AZ Insurance Stands Apart

AZ Insurance Agency has operated in the Houston area since 2003. 15 local offices. Bilingual service in English and Spanish. More than two decades of helping Houston-area homeowners understand what their policies actually say — not just what they think the policy says.

The wind/hail deductible conversation is one we have dozens of times every month. Not because it is a clever sales point. Because it is the single most consistent gap between what homeowners expect their insurance to do and what it actually does when a storm claim comes in.

Here is what working with AZ looks like for a homeowner who wants to close that gap:

We pull your current Declarations Page with you. We find the wind/hail deductible. We calculate the dollar exposure in plain numbers

We compare 8 carriers side by side — not just premium, but deductible structure, replacement cost provisions, extended replacement cost options, and wind/hail endorsement availability

We show you the tradeoffs in writing. If a flat-dollar wind deductible is available through another carrier at a higher premium, we show you the math. You decide

We re-shop at every renewal. Carrier pricing shifts every year. A better wind/hail structure that was not available 18 months ago may be available today

Some things to ask any agent before you commit to a homeowners policy:

What is the wind/hail deductible, expressed in dollars at my current Coverage A amount?

Does this carrier offer a flat-dollar wind deductible option, and what does it cost?

Is my Coverage A amount sufficient to rebuild my home at today's construction costs?

Are there separate hurricane and wind/hail deductibles, or is it one deductible for both?

What endorsements would lower my out-of-pocket exposure on a storm claim?

If your current agent cannot answer all five questions in about five minutes, that is information worth acting on.

Getting a homeowners insurance quote through AZ takes less than thirty minutes and compares eight carriers across all of these variables at once. A free coverage review — for homeowners who already have a policy and just want to understand what it actually says — costs nothing and requires only your current Declarations Page.

Houston storms are not a matter of if. They are a matter of when. The wind/hail deductible conversation is a thirty-minute conversation that could save you five, eight, or ten thousand dollars the next time a storm comes through. It is worth having before the clouds build.

Frequently Asked Questions

Q: My policy says my deductible is $1,000. Does that apply to hail damage?

Not necessarily. Most Texas homeowners policies carry two deductibles: a flat-dollar deductible for standard claims (fire, water, theft) and a separate percentage-based deductible for wind and hail. The $1,000 on your policy likely refers to the All Other Perils (AOP) deductible. Your Declarations Page will list the wind/hail or named storm deductible separately. Look for it before assuming the flat amount applies to storm damage.

Q: Is it legal for my carrier to charge me a 2% wind deductible without telling me?

The Texas Insurance Code requires carriers to disclose wind and hail deductibles clearly in the policy documents before the policy takes effect. The disclosure must appear on the Declarations Page. If you believe your carrier failed to disclose a percentage deductible, you can file a complaint with the Texas Department of Insurance at tdi.texas.gov. However, if the deductible is listed on your Declarations Page, it was disclosed — regardless of whether you read that page at signing.

Q: Can I negotiate my wind/hail deductible with my current carrier?

Some carriers offer endorsements that modify or cap the wind/hail deductible, often for an additional premium. Not all carriers offer this option, and availability varies by location and risk profile. The more practical approach is to shop the market — an independent agent who works with multiple carriers can find you a policy with a more favorable deductible structure than what your current carrier offers.

Q: My home is insured for $350,000 but I only paid $280,000 for it. Do I still have a $7,000 deductible?

Yes. Homeowners insurance deductibles are calculated against the dwelling's insured replacement value (Coverage A on your Declarations Page), not the purchase price or market value. The cost to rebuild a home after a total loss — materials, labor, permits — often significantly exceeds what a buyer paid for it, particularly in Houston's current construction cost environment. Your Coverage A amount should reflect what rebuilding would cost, not what you paid.

Q: What happens if storm damage comes in below my wind/hail deductible?

If the adjuster's damage estimate is less than your deductible, the carrier pays nothing. The loss is entirely your responsibility. Many smaller hail events — roof granule loss, minor gutter damage, cosmetic siding impact — produce claims in the $3,000 to $6,000 range that fall entirely below a 2% deductible on a $300,000+ home. This is one reason Texas homeowners are increasingly filing fewer small wind claims and banking deductible exposure against major events.

Q: Is AZ Insurance able to help if I already have a policy and just want to understand it?

Yes. A free coverage review is available regardless of whether you are currently an AZ policyholder. Bring your Declarations Page and AZ can walk through the deductible structure, Coverage A adequacy, available endorsements, and what the open market looks like for your home. There is no obligation to switch. The goal is that you leave the conversation knowing exactly what your policy does and does not do.

Reviewed by AZ Insurance Agency, licensed in Texas, serving Houston since 2003. AZ Insurance compares 8 carriers per quote across Houston, Sugar Land, Katy, and the greater metro area.

The storm came through on a Tuesday afternoon. By Thursday morning the adjuster was standing in the driveway, photographing the roof and the fence and the side of the house where the siding had peeled back. By the following Monday there was a claims summary in the inbox: covered damage totaling $9,400. And then, a number no one had prepared for.

The deductible: $7,800.

Not the $1,000 the homeowner remembered from when they signed the policy. Not the $500 they vaguely recalled discussing at the kitchen table years ago. $7,800 — because the home was insured for $390,000 and the wind/hail deductible on the policy was 2 percent of the insured dwelling value.

Two percent sounds almost harmless. Two percent sounds like rounding error. Two percent on a Texas home is not $200. In most cases it is not even close.

This is the most expensive misunderstanding in homeowners insurance in Texas today. And it is almost always discovered at the exact moment it does the most damage: after a storm, when the claim is already in motion and there is nothing left to negotiate.

What Most Texas Homeowners Believe About Their Deductible

Ask a homeowner in the Houston suburbs what their deductible is and most of them will give you a flat number. $1,000. $2,500. Maybe $500 if they bought the policy when rates were lower. That flat number is what they remember from the application, from the agent conversation, from the disclosure they signed three or four years ago and have not thought about since.

That flat number is real. It appears on the policy. It applies to most claims.

But it does not apply to wind or hail.

In Texas, homeowners insurance policies routinely carry a second deductible — a separate, higher deductible that applies specifically when the damage is caused by wind, hail, or a named storm. This second deductible is expressed as a percentage of the home's insured value, not as a flat dollar amount.

Here is what that looks like in practice:

$300,000 insured home with a 2% wind/hail deductible: $6,000 out of pocket before the carrier pays anything

$350,000 insured home with a 2% wind/hail deductible: $7,000 out of pocket

$400,000 insured home with a 2% wind/hail deductible: $8,000 out of pocket

$450,000 insured home with a 2% wind/hail deductible: $9,000 out of pocket

$500,000 insured home with a 2% wind/hail deductible: $10,000 out of pocket

Suburban Houston, Sugar Land, and Katy are densely concentrated with homes in exactly this price range. A 2% deductible at these values is not a minor cost-sharing mechanism. It is a five-figure gap between what the policy covers and what lands in the homeowner's hands.

And in Texas, storm season is not an abstract risk. It is a recurring annual event.

Why Texas Policies Work This Way

Texas sits in one of the most active storm corridors in the country. The state absorbs more hurricane activity than any other continental state, and the interior corridor — including the entire greater Houston metro — sees severe thunderstorm and hail events that routinely cost insurers hundreds of millions of dollars in a single season.

Carriers responded to this exposure years ago by restructuring deductibles. Instead of absorbing the first $1,000 of every wind and hail claim, they began shifting more of the initial loss to homeowners through percentage-based deductibles. This allowed them to continue offering coverage in Texas at all — without it, many carriers would have simply exited the state, which some have done anyway.

What this means for homeowners:

The flat deductible (also called the All Other Perils or AOP deductible) still applies to water damage, theft, fire, and most non-wind events

The wind/hail deductible (also called the Named Storm Deductible on some policies) applies whenever wind or hail is the primary cause of loss

Both deductibles appear in the same policy — one document, two separate deductible structures, and most people only ever notice the first one

The Texas Insurance Code requires carriers to disclose percentage deductibles clearly in the policy documents. The law is on the homeowner's side. The problem is not disclosure — the problem is that most homeowners do not read their Declarations Page until they have a reason to, and by then it is often after a loss.

Where To Find Your Wind/Hail Deductible Right Now

You do not need to wait for a storm to find out what your exposure is. The information is already in your policy.

Pull out your homeowners insurance Declarations Page — it is the one-to-two-page summary that comes at the beginning of your policy document. It is also available through your carrier's online portal if you have one. Once you have it, look for any of these labels:

Wind/Hail Deductible

Named Storm Deductible

Hurricane Deductible

Windstorm Deductible

Wind Percentage Deductible

The value next to that label will be expressed either as a percentage (1%, 2%, 3%) or, if you have a carrier that offers it, as a flat dollar amount. If it is a percentage, multiply it by your dwelling coverage amount — the Coverage A figure on the same page — and that is your out-of-pocket exposure for any wind or hail claim.

A few things to check while you have the page open:

Is your Coverage A amount current? If you bought your home several years ago and have not updated your dwelling coverage, your insured value may be below what it would cost to rebuild the home today. That affects your deductible math and your claim payout

Is the deductible 1%, 2%, or higher? Some Texas policies carry 3% or even 5% wind/hail deductibles, particularly in coastal and near-coastal areas

Is there a separate hurricane deductible? Some policies split wind/hail and hurricane into two separate percentage deductibles

What is the effective trigger? Some named storm deductibles only activate when a storm is officially named by the National Hurricane Center — an important distinction for inland hail events

If anything on that page is unclear, that is exactly what an independent agent is for. At AZ Insurance, a coverage review costs nothing and takes about twenty minutes.

The Moment Most Homeowners Find Out — and Why It Is Too Late

Here is the pattern AZ Insurance sees repeatedly.

A storm moves through the Houston area in spring or early summer. Hail hits the northwest suburbs. Damage is widespread. The homeowner files a claim. The adjuster comes out, documents the roof damage, the gutters, potentially the siding, and produces a damage estimate. Let's say that estimate comes in at $9,000.

The homeowner is relieved. Nine thousand dollars covers a new roof. They start calling roofers.

Then the Explanation of Benefits arrives. The carrier has applied the wind/hail deductible. The home is insured for $450,000. The deductible is 2%. That is $9,000. The claim payout: $0. Or close to it. The carrier owes nothing until the damage exceeds the deductible — and in this case they are exactly equal.

The homeowner now owes the full cost of the roof repair out of pocket, with no reimbursement, on a policy they have paid premiums on for years.

This is not fraud. This is not the carrier acting in bad faith. This is a contractual structure the homeowner agreed to and, in most cases, never fully understood. The Texas Insurance Code required disclosure. The disclosure happened. The homeowner signed and moved on.

The remedy is not outrage after the claim. The remedy is reading the policy before the storm.

Can You Get a Flat-Dollar Wind/Hail Deductible in Texas?

Yes — but it comes at a cost, and availability depends heavily on which carrier you are with and where your home is located.

Some Texas homeowners insurers offer flat-dollar wind/hail deductible options. Instead of 2% of the insured value, the policy might offer a $5,000 or $10,000 flat deductible for wind and hail. In some cases you can buy the deductible down to $2,500 with an endorsement.

The tradeoff is premium. Flat-dollar wind deductibles transfer more of the initial loss back to the carrier. Carriers price that risk into the annual premium. Depending on your home value, risk profile, and the carrier, a flat-dollar wind deductible might cost you an additional $200 to $600 per year.

Whether that is worth it depends on the math:

On a $400,000 home with a 2% deductible: your wind/hail exposure is $8,000. If you can cap that at $5,000 flat for an extra $300/year, you are buying down $3,000 of risk for $300. That is a 10-to-1 leverage ratio. Most financial planners would call that a good trade

On a $250,000 home with a 2% deductible: your wind/hail exposure is $5,000. Paying $400/year extra to bring that to $2,500 flat means you need to file a wind claim within 6 years to break even. Depending on your neighborhood's storm history, that may or may not pencil

The calculation is different for every household. It depends on the home's value, the premium differential available in the market, the carrier options in your area, and how much liquidity you have if a major storm claim comes in.

This is exactly the kind of comparison that shopping across multiple carriers makes possible. The flat-dollar option your current carrier does not offer might be available through a different one — at a premium you can absorb.

What the Texas Department of Insurance Says About These Deductibles

The Texas Department of Insurance (TDI) regulates homeowners insurance in Texas and has issued clear guidance on wind and hail deductibles. Per TDI:

Carriers are required to clearly disclose wind/hail and named storm deductibles in the policy documents before the policy is issued

The Declarations Page must prominently list the deductible amount and the method by which it is calculated (percentage of Coverage A is the most common)

Carriers cannot add a wind/hail deductible mid-term without providing advance written notice and the right to cancel

Homeowners have the right to request a plain-language explanation of how any percentage deductible will be calculated in the event of a claim

The TDI Consumer Guide to Homeowners Insurance (tdi.texas.gov/consumer/homeins.html) and the dedicated windstorm insurance page (tdi.texas.gov/consumer/windstorm.html) both contain information homeowners can reference when reviewing their policies or disputing a claim decision.

A few things TDI cannot do:

TDI cannot force a carrier to lower your deductible. The deductible is a contractual term. If you want different terms, you need a different policy or a different carrier

TDI cannot reverse a valid claim decision. If the damage falls below your deductible, the carrier owes nothing — this is not a claims handling error, it is the policy working as written

TDI cannot shop the market for you. That is what an independent agent does

Knowing your rights under Texas Insurance Code is useful. It will not replace the knowledge gap between what your current policy says and what better options look like on the open market.

Why AZ Insurance Stands Apart

AZ Insurance Agency has operated in the Houston area since 2003. 15 local offices. Bilingual service in English and Spanish. More than two decades of helping Houston-area homeowners understand what their policies actually say — not just what they think the policy says.

The wind/hail deductible conversation is one we have dozens of times every month. Not because it is a clever sales point. Because it is the single most consistent gap between what homeowners expect their insurance to do and what it actually does when a storm claim comes in.

Here is what working with AZ looks like for a homeowner who wants to close that gap:

We pull your current Declarations Page with you. We find the wind/hail deductible. We calculate the dollar exposure in plain numbers

We compare 8 carriers side by side — not just premium, but deductible structure, replacement cost provisions, extended replacement cost options, and wind/hail endorsement availability

We show you the tradeoffs in writing. If a flat-dollar wind deductible is available through another carrier at a higher premium, we show you the math. You decide

We re-shop at every renewal. Carrier pricing shifts every year. A better wind/hail structure that was not available 18 months ago may be available today

Some things to ask any agent before you commit to a homeowners policy:

What is the wind/hail deductible, expressed in dollars at my current Coverage A amount?

Does this carrier offer a flat-dollar wind deductible option, and what does it cost?

Is my Coverage A amount sufficient to rebuild my home at today's construction costs?

Are there separate hurricane and wind/hail deductibles, or is it one deductible for both?

What endorsements would lower my out-of-pocket exposure on a storm claim?

If your current agent cannot answer all five questions in about five minutes, that is information worth acting on.

Getting a homeowners insurance quote through AZ takes less than thirty minutes and compares eight carriers across all of these variables at once. A free coverage review — for homeowners who already have a policy and just want to understand what it actually says — costs nothing and requires only your current Declarations Page.

Houston storms are not a matter of if. They are a matter of when. The wind/hail deductible conversation is a thirty-minute conversation that could save you five, eight, or ten thousand dollars the next time a storm comes through. It is worth having before the clouds build.

Frequently Asked Questions

Q: My policy says my deductible is $1,000. Does that apply to hail damage?

Not necessarily. Most Texas homeowners policies carry two deductibles: a flat-dollar deductible for standard claims (fire, water, theft) and a separate percentage-based deductible for wind and hail. The $1,000 on your policy likely refers to the All Other Perils (AOP) deductible. Your Declarations Page will list the wind/hail or named storm deductible separately. Look for it before assuming the flat amount applies to storm damage.

Q: Is it legal for my carrier to charge me a 2% wind deductible without telling me?

The Texas Insurance Code requires carriers to disclose wind and hail deductibles clearly in the policy documents before the policy takes effect. The disclosure must appear on the Declarations Page. If you believe your carrier failed to disclose a percentage deductible, you can file a complaint with the Texas Department of Insurance at tdi.texas.gov. However, if the deductible is listed on your Declarations Page, it was disclosed — regardless of whether you read that page at signing.

Q: Can I negotiate my wind/hail deductible with my current carrier?

Some carriers offer endorsements that modify or cap the wind/hail deductible, often for an additional premium. Not all carriers offer this option, and availability varies by location and risk profile. The more practical approach is to shop the market — an independent agent who works with multiple carriers can find you a policy with a more favorable deductible structure than what your current carrier offers.

Q: My home is insured for $350,000 but I only paid $280,000 for it. Do I still have a $7,000 deductible?

Yes. Homeowners insurance deductibles are calculated against the dwelling's insured replacement value (Coverage A on your Declarations Page), not the purchase price or market value. The cost to rebuild a home after a total loss — materials, labor, permits — often significantly exceeds what a buyer paid for it, particularly in Houston's current construction cost environment. Your Coverage A amount should reflect what rebuilding would cost, not what you paid.

Q: What happens if storm damage comes in below my wind/hail deductible?

If the adjuster's damage estimate is less than your deductible, the carrier pays nothing. The loss is entirely your responsibility. Many smaller hail events — roof granule loss, minor gutter damage, cosmetic siding impact — produce claims in the $3,000 to $6,000 range that fall entirely below a 2% deductible on a $300,000+ home. This is one reason Texas homeowners are increasingly filing fewer small wind claims and banking deductible exposure against major events.

Q: Is AZ Insurance able to help if I already have a policy and just want to understand it?

Yes. A free coverage review is available regardless of whether you are currently an AZ policyholder. Bring your Declarations Page and AZ can walk through the deductible structure, Coverage A adequacy, available endorsements, and what the open market looks like for your home. There is no obligation to switch. The goal is that you leave the conversation knowing exactly what your policy does and does not do.

Latest Blogs

Are You Underinsured? How Much Dwelling Coverage Your Houston Home Needs

What Is Business Personal Property Insurance Coverage and Why Does It Matter?

Your Roof and Texas Home Insurance: Age, Depreciation, and Nonrenewal

Sole Proprietor Business Insurance: Common Risks and How to Protect Yourself

Actual Cash Value vs Replacement Cost: What Every Texas Homeowner Needs to Know Before the Next Storm

Does Your Health Insurance Work Abroad? A Houston Guide

Let A-Z Auto Insurance Help You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto Insurance Help

You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto

Insurance Help You

Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto Insurance Help

You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Latest New & Blogs

Latest New & Blogs

Related Blog Posts

Related Blog Posts

Your Roof and Texas Home Insurance: Age, Depreciation, and Nonrenewal

Roof age is one of the biggest factors Texas carriers use to set premiums and decide coverage. Here is what Houston homeowners need to know before their next renewal.

Your Roof and Texas Home Insurance: Age, Depreciation, and Nonrenewal

Roof age is one of the biggest factors Texas carriers use to set premiums and decide coverage. Here is what Houston homeowners need to know before their next renewal.

Your Roof and Texas Home Insurance: Age, Depreciation, and Nonrenewal

Roof age is one of the biggest factors Texas carriers use to set premiums and decide coverage. Here is what Houston homeowners need to know before their next renewal.

Sole Proprietor Business Insurance: Common Risks and How to Protect Yourself

What is the sole proprietor for business insurance, and do you need it? Learn the biggest risks, coverage types, & how to protect your Texas sole proprietorship.

Sole Proprietor Business Insurance: Common Risks and How to Protect Yourself

What is the sole proprietor for business insurance, and do you need it? Learn the biggest risks, coverage types, & how to protect your Texas sole proprietorship.

Sole Proprietor Business Insurance: Common Risks and How to Protect Yourself

What is the sole proprietor for business insurance, and do you need it? Learn the biggest risks, coverage types, & how to protect your Texas sole proprietorship.

Actual Cash Value vs Replacement Cost: What Every Texas Homeowner Needs to Know Before the Next Storm

ACV pays the depreciated value of your roof or belongings. Replacement cost pays to rebuild new. Texas storm numbers show the gap can be thousands.

Actual Cash Value vs Replacement Cost: What Every Texas Homeowner Needs to Know Before the Next Storm

ACV pays the depreciated value of your roof or belongings. Replacement cost pays to rebuild new. Texas storm numbers show the gap can be thousands.

Actual Cash Value vs Replacement Cost: What Every Texas Homeowner Needs to Know Before the Next Storm

ACV pays the depreciated value of your roof or belongings. Replacement cost pays to rebuild new. Texas storm numbers show the gap can be thousands.

Your Roof and Texas Home Insurance: Age, Depreciation, and Nonrenewal

Roof age is one of the biggest factors Texas carriers use to set premiums and decide coverage. Here is what Houston homeowners need to know before their next renewal.

Sole Proprietor Business Insurance: Common Risks and How to Protect Yourself

What is the sole proprietor for business insurance, and do you need it? Learn the biggest risks, coverage types, & how to protect your Texas sole proprietorship.