Quick support from trusted insurance professionals Call +1 713-777-2886 today!

Quick professional support Call +1 713-777-2886 today!

Quick professional support Call +1 713-777-2886 today!

Table of Content

Title

Let AZ Insurance Help You

Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto Insurance Help You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

The Cost of Motorcycle Insurance Claims - AZ Insurance Agency

The Cost of Motorcycle Insurance Claims - AZ Insurance Agency

The Cost of Motorcycle Insurance Claims - AZ Insurance Agency

The Cost of Motorcycle Insurance Claims - AZ Insurance Agency

The Cost of Motorcycle Insurance Claims - AZ Insurance Agency

11:36 AM

11:36 AM

Just like with car insurance, motorcycle insurance premiums may go up after an accident. Certain claims are more costly than others, however. While you drive as carefully and defensively as possible, it’s not always possible to avoid an accident, so it’s important to know how it will affect your motorcycle insurance rates.

Location Matters

Keep in mind that premium changes even for the same accident can vary depending on what state the bike is insured in. A traffic violation in one state may cost you differently than the same traffic violation in another, so be sure to keep tabs on the changes specific to your state.

At-Fault Accidents

At-fault accidents are basic accidents where the insured driver is ruled the cause. Most states are fault states, meaning that the driver who caused the accident is responsible for the injuries and damages. This is where motorcycle insurance comes in to shoulder some of the cost.

A single at-fault accident in most states may raise your rates by 50% or less. This can be hundreds of dollars or even a thousand in difference from your base rate. Premium changes are also often calculated based on the amount of damage caused. Accidents that involve more expensive damages usually raise your motorcycle insurance premiums by more.

DUIs and DWIs

DUIs are seen as one of the more serious offenses in most states. In most places, DUIs can raise your motorcycle insurance rates by 80% or more. DUIs and DWIs may last on your driving record for around 10 years, depending on where you live.

Tickets and Traffic Violations

Traffic and moving violations affect your motorcycle insurance at a lower rate, but they can still raise your premiums by a significant amount. Many of these violations raise rates by 20%-30%.

Do Accidents Always Raise Motorcycle Insurance Rates?

Contrary to popular belief, accidents don’t always raise motorcycle insurance rates. Many insurance agencies offer accident forgiveness, especially when it comes to accidents that are not determined to be the driver’s fault. Accidents caused by other drivers may not raise your motorcycle insurance rates. If you’re concerned about an accident raising your rates, be sure to look for an insurance provider that offers accident forgiveness. Many are especially lenient if the driver has no previous claims or accidents.

Do Car Accidents Affect Motorcycle Insurance Rates?

All vehicle accidents that affect your driving record also affect your motorcycle insurance rates. Even if you have an accident in your car, your motorcycle insurance rates may go up. This is because the insurance agency considers the elevated risk of you filing another claim, whether while operating your car or operating your motorcycle. Drivers with more previous violations or claims are seen as more likely to have another accident or file another claim. In order to compensate for that risk, insurance agencies charge more.

How Far Back Do Motorcycle Insurance Agencies Look?

Insurance agencies generally look back around 3 to 5 years on your driving record. Certain violations remain on your record for longer, depending on the severity of the accident and damage.

This is why it’s best to drive defensively and avoid distractions. Before filing a claim, also consider the damages to your vehicle in comparison to the deductible. If the damages cost less to repair than the price of your deductible, it may be more cost-effective to pay for the damages out of pocket rather than file an insurance claim. On the other hand, substantial damages that cost much more than the price of your motorcycle insurance deductible may be better covered under a claim.

Just like with car insurance, motorcycle insurance premiums may go up after an accident. Certain claims are more costly than others, however. While you drive as carefully and defensively as possible, it’s not always possible to avoid an accident, so it’s important to know how it will affect your motorcycle insurance rates.

Location Matters

Keep in mind that premium changes even for the same accident can vary depending on what state the bike is insured in. A traffic violation in one state may cost you differently than the same traffic violation in another, so be sure to keep tabs on the changes specific to your state.

At-Fault Accidents

At-fault accidents are basic accidents where the insured driver is ruled the cause. Most states are fault states, meaning that the driver who caused the accident is responsible for the injuries and damages. This is where motorcycle insurance comes in to shoulder some of the cost.

A single at-fault accident in most states may raise your rates by 50% or less. This can be hundreds of dollars or even a thousand in difference from your base rate. Premium changes are also often calculated based on the amount of damage caused. Accidents that involve more expensive damages usually raise your motorcycle insurance premiums by more.

DUIs and DWIs

DUIs are seen as one of the more serious offenses in most states. In most places, DUIs can raise your motorcycle insurance rates by 80% or more. DUIs and DWIs may last on your driving record for around 10 years, depending on where you live.

Tickets and Traffic Violations

Traffic and moving violations affect your motorcycle insurance at a lower rate, but they can still raise your premiums by a significant amount. Many of these violations raise rates by 20%-30%.

Do Accidents Always Raise Motorcycle Insurance Rates?

Contrary to popular belief, accidents don’t always raise motorcycle insurance rates. Many insurance agencies offer accident forgiveness, especially when it comes to accidents that are not determined to be the driver’s fault. Accidents caused by other drivers may not raise your motorcycle insurance rates. If you’re concerned about an accident raising your rates, be sure to look for an insurance provider that offers accident forgiveness. Many are especially lenient if the driver has no previous claims or accidents.

Do Car Accidents Affect Motorcycle Insurance Rates?

All vehicle accidents that affect your driving record also affect your motorcycle insurance rates. Even if you have an accident in your car, your motorcycle insurance rates may go up. This is because the insurance agency considers the elevated risk of you filing another claim, whether while operating your car or operating your motorcycle. Drivers with more previous violations or claims are seen as more likely to have another accident or file another claim. In order to compensate for that risk, insurance agencies charge more.

How Far Back Do Motorcycle Insurance Agencies Look?

Insurance agencies generally look back around 3 to 5 years on your driving record. Certain violations remain on your record for longer, depending on the severity of the accident and damage.

This is why it’s best to drive defensively and avoid distractions. Before filing a claim, also consider the damages to your vehicle in comparison to the deductible. If the damages cost less to repair than the price of your deductible, it may be more cost-effective to pay for the damages out of pocket rather than file an insurance claim. On the other hand, substantial damages that cost much more than the price of your motorcycle insurance deductible may be better covered under a claim.

Latest Blogs

Information Needed for a Homeowners Insurance Quote Explained

NFIP Changes in 2026: Houston Homeowners Guide to Flood Insurance Options (Private vs Federal)

Does Your Houston Lease Require Renters Insurance? (What To Buy, How Much It Costs, Where To Get It Same-Day)

Does Homeowners Insurance Cover Flood in Texas? (The Answer Costs Houston Families Thousands)

How to Switch Car Insurance: A Step-by-Step Guide to Changing Companies or Moving States

Do You Need Insurance Before Registering a Car in Texas?

Let A-Z Auto Insurance Help You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto Insurance Help

You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto

Insurance Help You

Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto Insurance Help

You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Latest New & Blogs

Latest New & Blogs

Related Blog Posts

Related Blog Posts

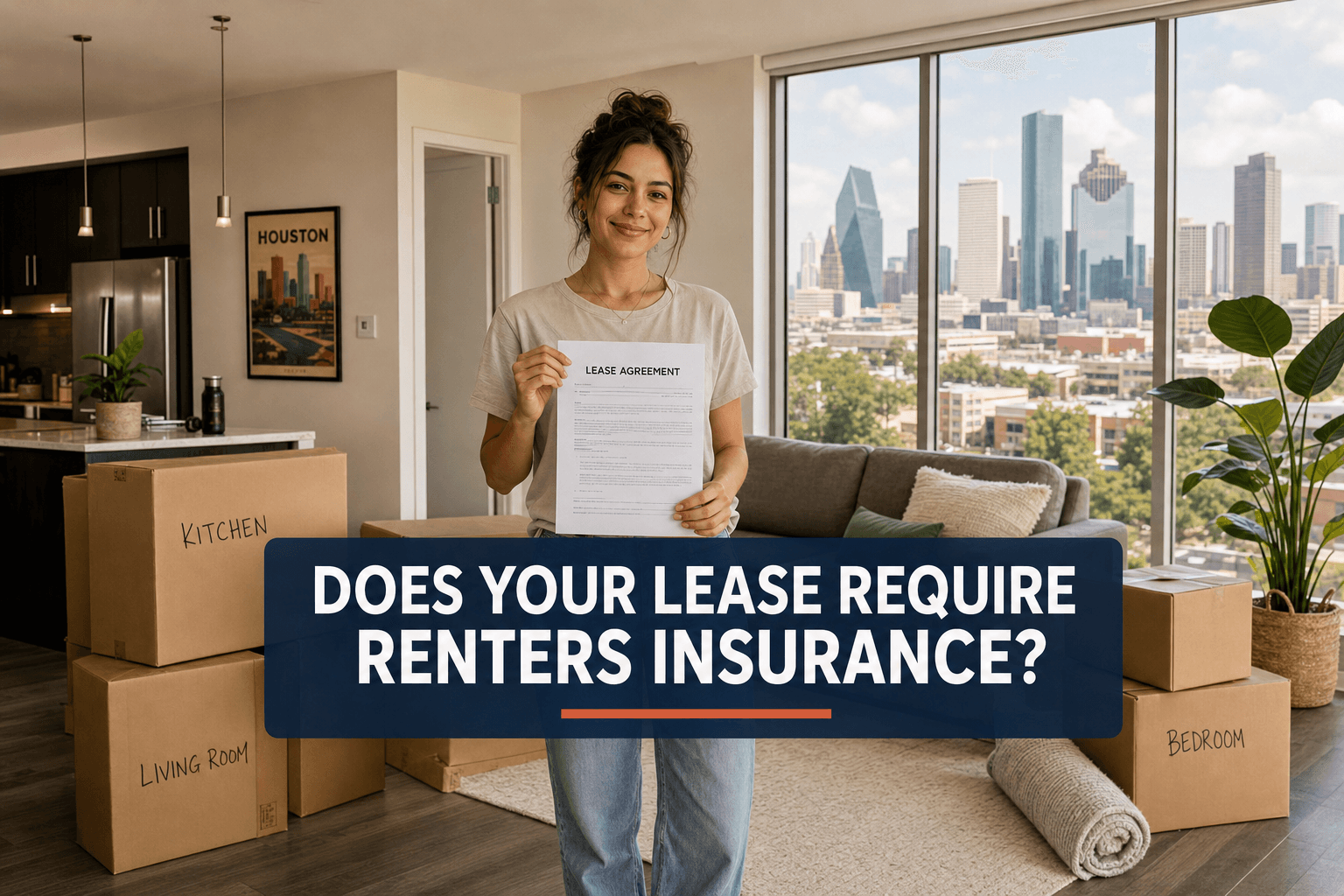

Does Your Houston Lease Require Renters Insurance? (What To Buy, How Much It Costs, Where To Get It Same-Day)

Most Houston leases now require renters insurance. Here's what the clause means, what to buy, what it costs, and how to get same-day proof at AZ Insurance.

Does Your Houston Lease Require Renters Insurance? (What To Buy, How Much It Costs, Where To Get It Same-Day)

Most Houston leases now require renters insurance. Here's what the clause means, what to buy, what it costs, and how to get same-day proof at AZ Insurance.

Does Your Houston Lease Require Renters Insurance? (What To Buy, How Much It Costs, Where To Get It Same-Day)

Most Houston leases now require renters insurance. Here's what the clause means, what to buy, what it costs, and how to get same-day proof at AZ Insurance.

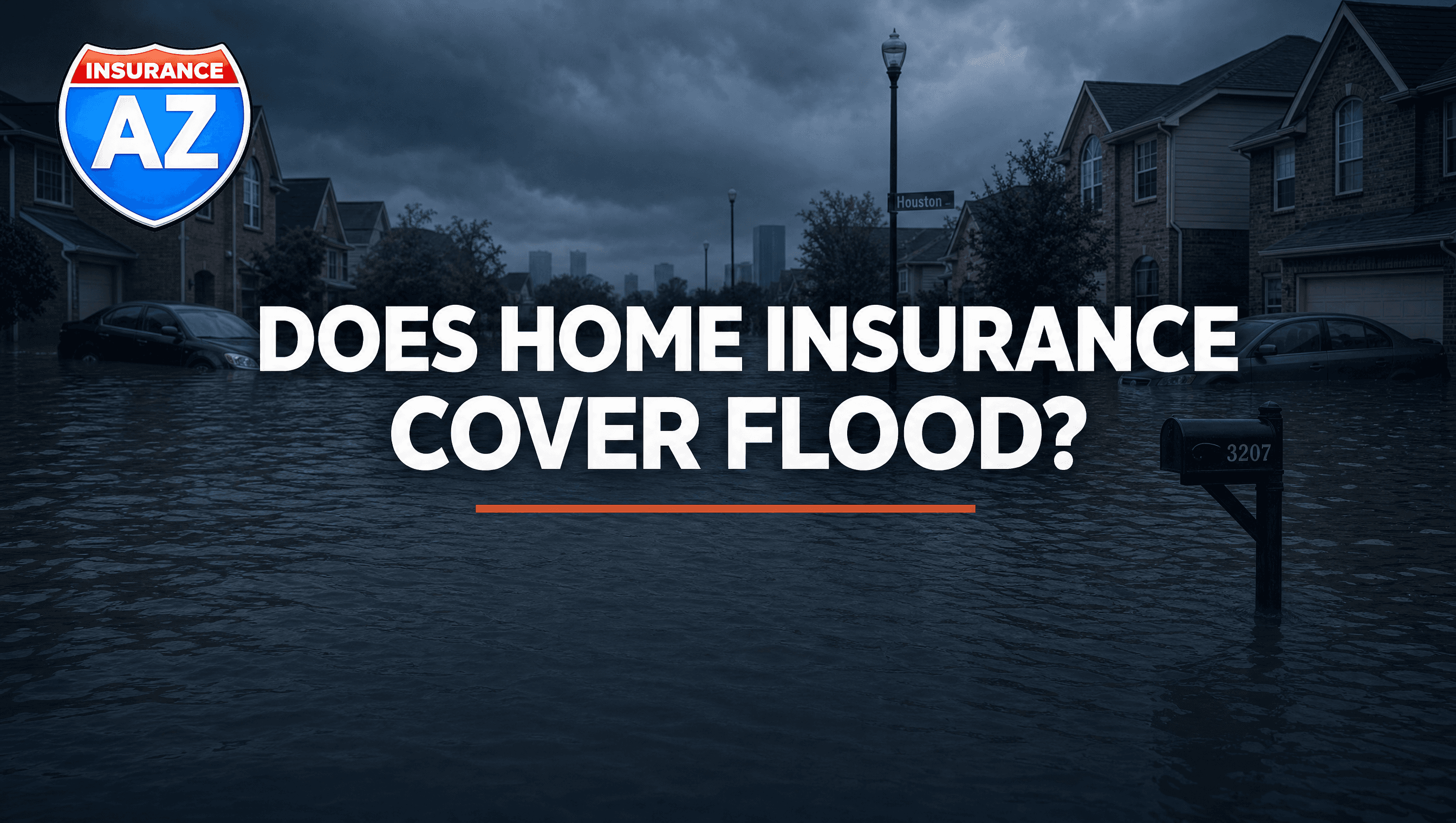

Does Homeowners Insurance Cover Flood in Texas? (The Answer Costs Houston Families Thousands)

Standard homeowners insurance never covers flood in Texas. With hurricane season open and a 30-day NFIP wait, the time to act is now — before a storm forms.

Does Homeowners Insurance Cover Flood in Texas? (The Answer Costs Houston Families Thousands)

Standard homeowners insurance never covers flood in Texas. With hurricane season open and a 30-day NFIP wait, the time to act is now — before a storm forms.

Does Homeowners Insurance Cover Flood in Texas? (The Answer Costs Houston Families Thousands)

Standard homeowners insurance never covers flood in Texas. With hurricane season open and a 30-day NFIP wait, the time to act is now — before a storm forms.

How to Switch Car Insurance: A Step-by-Step Guide to Changing Companies or Moving States

Learn how to switch car insurance companies easily, avoid coverage gaps, compare quotes, and save money with this step-by-step guide

How to Switch Car Insurance: A Step-by-Step Guide to Changing Companies or Moving States

Learn how to switch car insurance companies easily, avoid coverage gaps, compare quotes, and save money with this step-by-step guide

How to Switch Car Insurance: A Step-by-Step Guide to Changing Companies or Moving States

Learn how to switch car insurance companies easily, avoid coverage gaps, compare quotes, and save money with this step-by-step guide

Does Your Houston Lease Require Renters Insurance? (What To Buy, How Much It Costs, Where To Get It Same-Day)

Most Houston leases now require renters insurance. Here's what the clause means, what to buy, what it costs, and how to get same-day proof at AZ Insurance.

Does Homeowners Insurance Cover Flood in Texas? (The Answer Costs Houston Families Thousands)

Standard homeowners insurance never covers flood in Texas. With hurricane season open and a 30-day NFIP wait, the time to act is now — before a storm forms.