Quick support from trusted insurance professionals Call +1 713-777-2886 today!

Quick professional support Call +1 713-777-2886 today!

Quick professional support Call +1 713-777-2886 today!

Table of Content

Title

Let AZ Insurance Help You

Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto Insurance Help You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

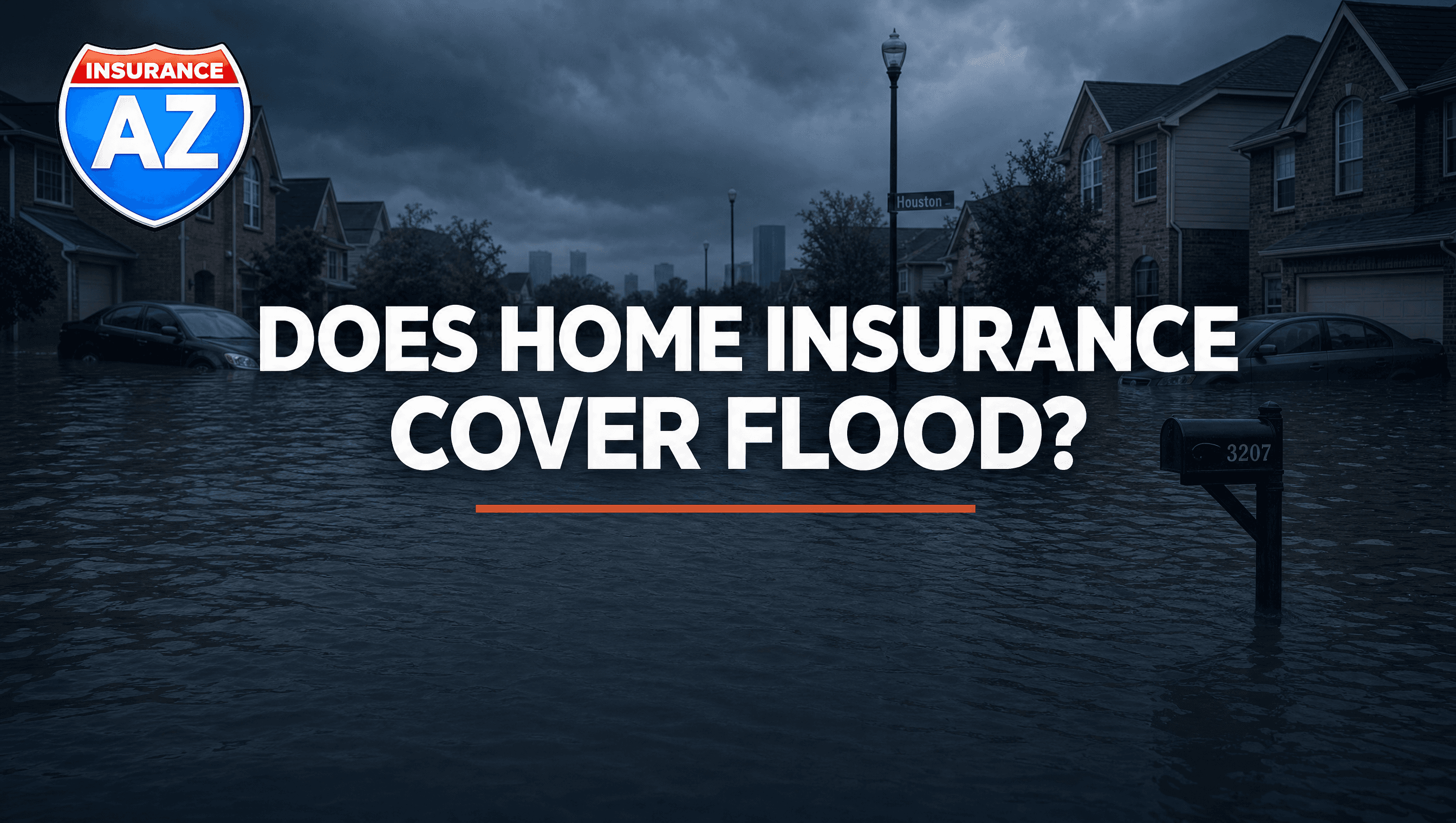

Does Homeowners Insurance Cover Flood in Texas? (The Answer Costs Houston Families Thousands)

Does Homeowners Insurance Cover Flood in Texas? (The Answer Costs Houston Families Thousands)

Does Homeowners Insurance Cover Flood in Texas? (The Answer Costs Houston Families Thousands)

Does Homeowners Insurance Cover Flood in Texas? (The Answer Costs Houston Families Thousands)

Does Homeowners Insurance Cover Flood in Texas? (The Answer Costs Houston Families Thousands)

Reviewed by AZ Insurance Agency, licensed in Texas, serving Houston since 2003.

Every year, a few weeks after a major flood event, we get the same call at our offices. A homeowner. Water in the house. Sometimes a foot. Sometimes three feet. They filed a claim with their homeowners insurance carrier. The carrier sent a letter. The letter says: flood damage is not covered under your policy.

They had no idea.

This is not a paperwork technicality. This is not something that slipped through a loophole. Flood is categorically excluded from every standard homeowners insurance policy written in Texas — and in every other state. It has been that way for decades. Yet as of today, roughly 85% of Texas homeowners are carrying no flood coverage at all. In Harris County — the county that has sustained more flood damage than any other county in the United States — the majority of homeowners are one storm away from a six-figure loss with no safety net.

Hurricane season opened June 1. The NFIP — the federal flood insurance program — carries a mandatory 30-day waiting period before coverage activates. That means a homeowner who buys flood insurance today has a real chance of being protected before the first named storm of the season threatens the Texas coast. A homeowner who waits until they see a storm forming on the radar will not be covered.

This is the conversation every Houston homeowner needs to have this week. Not next month. This week.

If you want to start now, you can request a homeowners insurance quote with flood options from AZ Insurance and our team will walk you through exactly where you stand.

What Standard Homeowners Insurance Actually Covers (And What It Does Not)

A standard Texas homeowners policy — the HO-3, which is the policy form most Texas homeowners carry — is designed around one specific type of water damage: sudden, accidental water that originates from inside the home. It is not designed around water that originates from outside the home and enters due to weather.

The Texas Department of Insurance is explicit about this. Standard homeowners insurance covers losses from things like:

A pipe bursting inside your wall and water flooding your floors

A washing machine hose failing and soaking your laundry room

A roof leak caused by wind during a covered storm (with conditions)

Hail damage to your roof and exterior

Fire, lightning, theft, and vandalism

Standard homeowners insurance does NOT cover:

Rising water from a river, bayou, creek, or drainage channel overflowing

Storm surge pushing ocean or bay water inland and into your home

Sheet flooding from heavy rainfall overwhelming drainage systems

Groundwater entering through your foundation, walls, or lower level

Overland flooding from any source, regardless of what caused it

The distinction the industry draws is between "water from above" (rain hitting your roof, which your policy may cover in limited ways) and "water from below or outside" (flooding, which your policy will not cover, period). When a hurricane or tropical storm drops 10, 20, or 50 inches of rain on Houston in a matter of days — as Harvey did in August 2017 — the water that enters homes does not come through the roof. It comes through the streets, the drainage systems, the bayous, the yards, and ultimately the doors, walls, and floors. That is flood. That is excluded.

This is not negotiable. This is not something you can argue with your carrier after the fact. It is written into the policy form and it will not change based on the severity of the event or the amount of damage you sustained. For a complete breakdown of which losses a Texas homeowners policy does and does not pay for, see our guide to what homeowners insurance covers and does not cover.

What Hurricane Harvey Actually Cost Houston Homeowners

Harvey made landfall in August 2017 and stalled over Southeast Texas for four days, dropping a record 60+ inches of rain in some locations. More than 150,000 homes in the Houston area were damaged or destroyed. The total economic damage exceeded $125 billion, making Harvey the costliest natural disaster in U.S. history at the time.

The average flood claim paid by NFIP after Harvey was over $60,000.

That number needs to land. The average family filing a flood claim — not an extreme case, not a total loss, the average — received more than sixty thousand dollars. And tens of thousands of Houston homeowners who were flooded received nothing because they had no flood coverage.

FEMA's own post-Harvey data showed that the majority of flooded homes in Harris County were outside the FEMA Special Flood Hazard Area — the 100-year flood plain that most people think of as "the flood zone." Meaning: they were homeowners who had been told, or had assumed, that their flood risk was low. They were wrong. So was the map.

The lesson Houston had to learn the hard way is this: flood risk in Harris County is not confined to the lines on a FEMA map. It is systemic. The region sits at near-sea level. The clay soil absorbs almost no water. The bayou and drainage systems that handle normal rainfall cannot handle a major storm event. The entire metro area floods when the storms are large enough — and in a warming Gulf, the storms are getting larger. That same warming trend is reshaping exposure for businesses too, which we cover in climate risk and commercial insurance.

The NFIP: What Federal Flood Insurance Covers (And Its Limits)

The National Flood Insurance Program is a federal program administered by FEMA. It was created in 1968 specifically because private insurers had largely exited the flood market — flood losses were too severe and too concentrated geographically for standard private underwriting.

NFIP policies are sold through private insurance agents, including our team at AZ Insurance, but the coverage itself is backed by the federal government. The Texas Department of Insurance and FEMA both provide resources to help homeowners understand NFIP eligibility.

Here is what NFIP flood insurance covers:

Building/Structure coverage: Up to $250,000 for the physical structure of your home — foundation, walls, floors, electrical systems, plumbing, HVAC, built-in appliances, and more

Contents coverage: Up to $100,000 for personal belongings inside the home — furniture, clothing, electronics, and other personal property

Both coverages are separate policies — you can purchase one or both

Here is what NFIP flood insurance does NOT cover:

Losses above the coverage maximums ($250K structure / $100K contents)

Additional living expenses if you are displaced from your home during repairs

Landscaping, decks, patios, fences, or detached structures (in most cases)

Vehicles (covered separately under comprehensive auto insurance)

Financial losses, business income, or other consequential damages

The 30-day waiting period is perhaps the most operationally critical feature of NFIP. With narrow exceptions (purchasing at closing, following a FEMA map revision, or adding coverage following a lender requirement), a new NFIP policy does not activate until 30 days after purchase. If a named storm is already forming or is being tracked toward the Texas coast, it is too late to buy NFIP coverage and expect it to protect you from that storm.

For a home valued above $250,000 — which describes a large portion of Houston's housing stock — NFIP's $250,000 cap may be insufficient to cover a total or near-total loss. This is where private flood insurance becomes important — our deep dive on NFIP vs private flood insurance in Houston compares the two side by side. And if you run a business out of your home or own commercial property, flood works differently there: see commercial flood insurance in Houston, the difference between personal and commercial insurance, and how a business owners policy bundles the essentials.

Private Flood Insurance: Often Cheaper, Sometimes Broader

Private flood insurance has expanded significantly since Hurricane Katrina and Harvey accelerated market development. Today, several private carriers offer flood policies that differ from NFIP in meaningful ways:

Higher coverage limits: Private policies can cover homes valued well above $250,000, with no federal cap

Contents limits above $100K: For homeowners with significant personal property, private policies may offer higher contents protection

Shorter waiting periods: Some private flood insurers offer waiting periods as short as 10 to 14 days, compared to NFIP's 30 days

Additional living expenses: Some private policies include coverage for hotel and rental costs if you are displaced during repairs — NFIP does not

Broader definitions of flood: Some private policies cover scenarios NFIP policies do not

Competitive pricing: For lower-risk properties, private flood insurance is sometimes meaningfully cheaper than NFIP premiums

Private flood insurance is not right for every homeowner. For properties in high-risk flood zones, NFIP rates may be more competitive. For homeowners with federally-backed mortgages in mandatory purchase zones, lenders may require an NFIP policy specifically. But for many Houston homeowners, a private flood option is worth a side-by-side comparison.

At AZ Insurance, we compare options across 8 carriers to find the coverage that fits your home, your risk, and your budget. You can start with a free coverage review at any of our 14 Houston-area offices — same-day appointments are available.

Harris County: Why Houston Flood Risk Is Not What Most Homeowners Think

Harris County has sustained more flood damage than any other county in the United States. This is not a ranking based on one bad storm. It is a cumulative record built over decades of major flood events — Allison in 2001, Ike in 2008, the Tax Day Flood in 2016, Harvey in 2017, and a long series of significant flooding events before and between those storms.

The reasons are structural and geographic:

Elevation: Large portions of Harris County sit at or near sea level, giving floodwater little gradient to drain

Soil: The region's clay-heavy soil has extremely low permeability — rainfall sits on the surface rather than soaking in

Bayou network: Houston's bayou system, while extensive, was not engineered to handle the rainfall volumes that modern storm systems produce

Development: Decades of impervious surface expansion — roads, parking lots, rooftops — has reduced the land's natural ability to absorb runoff, accelerating flooding in downstream neighborhoods

Storm track: The Gulf of Mexico is warm, and warm Gulf water intensifies tropical systems rapidly. Storms that reach the Texas coast often arrive stronger and wetter than forecast

FEMA's flood maps, which designate "Special Flood Hazard Areas," are based on historical data and are updated infrequently. Harvey demonstrated conclusively that a majority of flooded homes were outside mapped flood hazard zones. In practical terms: being outside the 100-year flood plain in Harris County does not mean your flood risk is low. It means you are in a county that floods — and that your particular neighborhood has not flooded as recently or as deeply as mapped high-risk zones have.

Renters are not exempt from this risk. If you rent your home and a flood event damages or destroys the structure, your landlord's policy covers the building — not your belongings. A renters insurance quote with a conversation about flood options for personal property is worth having before June 1 passes. If you rent, it helps to know whether renters insurance is worth it, the key considerations before you choose your limits, and — if you have a young adult in their first apartment — why kids moving out need their own renters policy.

The 30-Day Waiting Period and Hurricane Season: The Math Every Houston Homeowner Needs to Do

Hurricane season runs June 1 through November 30. The Gulf of Mexico typically becomes its most active between late August and mid-October, but named storms have struck Texas in June and July. If you have not gotten your home and vehicles storm-ready yet, our hurricane season preparedness guide is a practical place to start.

The NFIP's 30-day waiting period means that coverage purchased today — in late May or early June — would activate approximately 30 days from the purchase date. Coverage purchased at the beginning of June would be active by early July, before the Gulf reaches peak season temperatures.

The waiting period is not waived for any named storm already being tracked. Once the National Hurricane Center issues advisories on a system targeting the Gulf or Texas coastline, it is too late. Carriers and FEMA are explicit: if a storm is being tracked and you attempt to purchase flood insurance, the waiting period still applies. You will not be covered for damage from that storm.

This is why the timing of this article matters. We are publishing this in early June 2026 — before the major storm season peak, before any named storms are being tracked toward Texas, and before it is too late. The homeowners who read this, act this week, and purchase flood insurance will have active coverage by early July. The homeowners who bookmark this article and wait until a storm forms will not.

The step is not complicated:

Call or walk into any of our 14 AZ Insurance offices

Tell us you want to review your homeowners policy and look at flood options

We will compare NFIP and private flood options for your property

You can have a policy bound the same day

No storm on the radar. No waiting for a news alert. No hoping your neighborhood stays dry. Just coverage.

What Flood Insurance Does Not Cover That Homeowners Forget

Even homeowners who do purchase flood insurance sometimes discover gaps after a claim. It is worth understanding what flood policies — both NFIP and many private options — typically do not cover, so you can plan accordingly:

Additional living expenses: NFIP does not pay for your hotel, temporary rental, or meals while your home is uninhabitable. Some private flood policies do; NFIP does not. This can represent tens of thousands of dollars out-of-pocket during a multi-month repair process

Detached structures: Most NFIP policies do not cover detached garages, sheds, fences, or pools under standard terms

Landscaping and hardscaping: Trees, shrubs, patios, driveways, and other outdoor improvements are generally not covered

Basement contents: NFIP limits coverage for items stored in basements, even with a contents policy. Furniture, electronics, and personal property kept below grade may have limited or no coverage

Currency, precious metals, and important papers: NFIP excludes these categories

Vehicles: Cars, trucks, and motorcycles damaged by flooding are covered under the comprehensive portion of your auto insurance policy, not under your flood insurance policy (if you are unsure how that side of your coverage works, here is the main purpose of auto insurance)

High-value items above policy limits: Jewelry, art, and collections above certain limits require separate scheduled coverage

Understanding these gaps before a loss — not after — is the point of a coverage review. Our team will walk through your full exposure so you are not surprised by what a policy does and does not cover. The same goes for the rest of your homeowners policy: our guides on staying out of the doghouse with home insurance, protecting your home through the holidays, and whether prefabricated homes require insurance cover the year-round basics.

Frequently Asked Questions

Q: My home is not in a flood zone. Do I still need flood insurance in Houston?

Yes. The majority of homes flooded during Harvey were outside FEMA-designated Special Flood Hazard Areas. Harris County's hydrology means that even low-risk zones can flood during major storm events. Flood zone designation determines whether your lender requires you to purchase flood insurance — it does not determine whether your home can flood.

Q: How much does flood insurance cost in Houston?

Flood insurance premiums vary based on your property's elevation, construction type, flood zone designation, coverage amounts, and whether you choose NFIP or a private carrier. NFIP rates in low-to-moderate risk zones are often lower than many homeowners expect. A coverage review with our team will give you actual numbers for your specific address. Request a homeowners insurance quote to get started.

Q: How long does it take for flood insurance to activate after I buy it?

NFIP policies have a standard 30-day waiting period before coverage activates. Some private flood insurers offer shorter waiting periods — in some cases as short as 10 to 14 days. If a storm is already being tracked, neither option will protect you from that specific storm. Act before the forecast changes.

Q: Can I buy flood insurance directly from the government?

You purchase NFIP policies through licensed insurance agents — not directly from FEMA. Our agents at AZ Insurance are authorized to write NFIP policies and can compare NFIP against private flood options to find the best fit for your home and budget.

Q: My lender is requiring me to buy flood insurance. What are my options?

If you have a federally-backed mortgage (FHA, VA, Fannie Mae, Freddie Mac) and your home is in a Special Flood Hazard Area, your lender is required by law to ensure you carry flood insurance. You can typically satisfy this requirement with either an NFIP policy or a qualifying private flood policy. We can help you navigate the lender requirements and find coverage that satisfies the mandate and fits your budget.

Q: Does homeowners insurance cover water damage from a hurricane?

It depends on the source. Wind-driven rain that penetrates a damaged roof during a hurricane may be covered under your homeowners policy — though wind and hail claims are usually subject to a separate percentage-based deductible that catches many homeowners off guard (we break this down in Texas Storm Deductible Explained). Floodwater that enters your home due to storm surge, rising bayous, or sheet flooding from rainfall is not covered — that requires a separate flood insurance policy. The distinction matters enormously because most of the damage from major Texas hurricanes comes from flooding, not from the wind itself.

Why AZ Insurance Stands Apart

AZ Insurance has been serving Houston homeowners since 2003. We have 14 offices across the Houston area, we serve families in English and Spanish, and when you walk in for a coverage review, we are comparing options from 8 carriers — not selling you the one product we happen to carry. On flood coverage, that means we can show you NFIP side-by-side with private flood alternatives and tell you honestly which one fits your home, your risk profile, and your budget. We have been through Harvey. We have seen what a gap in flood coverage costs a family. We do not want that conversation to happen to you after the water rises.

Request a free coverage review at your nearest AZ Insurance office today — same-day appointments are available at all 14 Houston-area locations.

Related Articles

Reviewed by AZ Insurance Agency, licensed in Texas, serving Houston since 2003.

Every year, a few weeks after a major flood event, we get the same call at our offices. A homeowner. Water in the house. Sometimes a foot. Sometimes three feet. They filed a claim with their homeowners insurance carrier. The carrier sent a letter. The letter says: flood damage is not covered under your policy.

They had no idea.

This is not a paperwork technicality. This is not something that slipped through a loophole. Flood is categorically excluded from every standard homeowners insurance policy written in Texas — and in every other state. It has been that way for decades. Yet as of today, roughly 85% of Texas homeowners are carrying no flood coverage at all. In Harris County — the county that has sustained more flood damage than any other county in the United States — the majority of homeowners are one storm away from a six-figure loss with no safety net.

Hurricane season opened June 1. The NFIP — the federal flood insurance program — carries a mandatory 30-day waiting period before coverage activates. That means a homeowner who buys flood insurance today has a real chance of being protected before the first named storm of the season threatens the Texas coast. A homeowner who waits until they see a storm forming on the radar will not be covered.

This is the conversation every Houston homeowner needs to have this week. Not next month. This week.

If you want to start now, you can request a homeowners insurance quote with flood options from AZ Insurance and our team will walk you through exactly where you stand.

What Standard Homeowners Insurance Actually Covers (And What It Does Not)

A standard Texas homeowners policy — the HO-3, which is the policy form most Texas homeowners carry — is designed around one specific type of water damage: sudden, accidental water that originates from inside the home. It is not designed around water that originates from outside the home and enters due to weather.

The Texas Department of Insurance is explicit about this. Standard homeowners insurance covers losses from things like:

A pipe bursting inside your wall and water flooding your floors

A washing machine hose failing and soaking your laundry room

A roof leak caused by wind during a covered storm (with conditions)

Hail damage to your roof and exterior

Fire, lightning, theft, and vandalism

Standard homeowners insurance does NOT cover:

Rising water from a river, bayou, creek, or drainage channel overflowing

Storm surge pushing ocean or bay water inland and into your home

Sheet flooding from heavy rainfall overwhelming drainage systems

Groundwater entering through your foundation, walls, or lower level

Overland flooding from any source, regardless of what caused it

The distinction the industry draws is between "water from above" (rain hitting your roof, which your policy may cover in limited ways) and "water from below or outside" (flooding, which your policy will not cover, period). When a hurricane or tropical storm drops 10, 20, or 50 inches of rain on Houston in a matter of days — as Harvey did in August 2017 — the water that enters homes does not come through the roof. It comes through the streets, the drainage systems, the bayous, the yards, and ultimately the doors, walls, and floors. That is flood. That is excluded.

This is not negotiable. This is not something you can argue with your carrier after the fact. It is written into the policy form and it will not change based on the severity of the event or the amount of damage you sustained. For a complete breakdown of which losses a Texas homeowners policy does and does not pay for, see our guide to what homeowners insurance covers and does not cover.

What Hurricane Harvey Actually Cost Houston Homeowners

Harvey made landfall in August 2017 and stalled over Southeast Texas for four days, dropping a record 60+ inches of rain in some locations. More than 150,000 homes in the Houston area were damaged or destroyed. The total economic damage exceeded $125 billion, making Harvey the costliest natural disaster in U.S. history at the time.

The average flood claim paid by NFIP after Harvey was over $60,000.

That number needs to land. The average family filing a flood claim — not an extreme case, not a total loss, the average — received more than sixty thousand dollars. And tens of thousands of Houston homeowners who were flooded received nothing because they had no flood coverage.

FEMA's own post-Harvey data showed that the majority of flooded homes in Harris County were outside the FEMA Special Flood Hazard Area — the 100-year flood plain that most people think of as "the flood zone." Meaning: they were homeowners who had been told, or had assumed, that their flood risk was low. They were wrong. So was the map.

The lesson Houston had to learn the hard way is this: flood risk in Harris County is not confined to the lines on a FEMA map. It is systemic. The region sits at near-sea level. The clay soil absorbs almost no water. The bayou and drainage systems that handle normal rainfall cannot handle a major storm event. The entire metro area floods when the storms are large enough — and in a warming Gulf, the storms are getting larger. That same warming trend is reshaping exposure for businesses too, which we cover in climate risk and commercial insurance.

The NFIP: What Federal Flood Insurance Covers (And Its Limits)

The National Flood Insurance Program is a federal program administered by FEMA. It was created in 1968 specifically because private insurers had largely exited the flood market — flood losses were too severe and too concentrated geographically for standard private underwriting.

NFIP policies are sold through private insurance agents, including our team at AZ Insurance, but the coverage itself is backed by the federal government. The Texas Department of Insurance and FEMA both provide resources to help homeowners understand NFIP eligibility.

Here is what NFIP flood insurance covers:

Building/Structure coverage: Up to $250,000 for the physical structure of your home — foundation, walls, floors, electrical systems, plumbing, HVAC, built-in appliances, and more

Contents coverage: Up to $100,000 for personal belongings inside the home — furniture, clothing, electronics, and other personal property

Both coverages are separate policies — you can purchase one or both

Here is what NFIP flood insurance does NOT cover:

Losses above the coverage maximums ($250K structure / $100K contents)

Additional living expenses if you are displaced from your home during repairs

Landscaping, decks, patios, fences, or detached structures (in most cases)

Vehicles (covered separately under comprehensive auto insurance)

Financial losses, business income, or other consequential damages

The 30-day waiting period is perhaps the most operationally critical feature of NFIP. With narrow exceptions (purchasing at closing, following a FEMA map revision, or adding coverage following a lender requirement), a new NFIP policy does not activate until 30 days after purchase. If a named storm is already forming or is being tracked toward the Texas coast, it is too late to buy NFIP coverage and expect it to protect you from that storm.

For a home valued above $250,000 — which describes a large portion of Houston's housing stock — NFIP's $250,000 cap may be insufficient to cover a total or near-total loss. This is where private flood insurance becomes important — our deep dive on NFIP vs private flood insurance in Houston compares the two side by side. And if you run a business out of your home or own commercial property, flood works differently there: see commercial flood insurance in Houston, the difference between personal and commercial insurance, and how a business owners policy bundles the essentials.

Private Flood Insurance: Often Cheaper, Sometimes Broader

Private flood insurance has expanded significantly since Hurricane Katrina and Harvey accelerated market development. Today, several private carriers offer flood policies that differ from NFIP in meaningful ways:

Higher coverage limits: Private policies can cover homes valued well above $250,000, with no federal cap

Contents limits above $100K: For homeowners with significant personal property, private policies may offer higher contents protection

Shorter waiting periods: Some private flood insurers offer waiting periods as short as 10 to 14 days, compared to NFIP's 30 days

Additional living expenses: Some private policies include coverage for hotel and rental costs if you are displaced during repairs — NFIP does not

Broader definitions of flood: Some private policies cover scenarios NFIP policies do not

Competitive pricing: For lower-risk properties, private flood insurance is sometimes meaningfully cheaper than NFIP premiums

Private flood insurance is not right for every homeowner. For properties in high-risk flood zones, NFIP rates may be more competitive. For homeowners with federally-backed mortgages in mandatory purchase zones, lenders may require an NFIP policy specifically. But for many Houston homeowners, a private flood option is worth a side-by-side comparison.

At AZ Insurance, we compare options across 8 carriers to find the coverage that fits your home, your risk, and your budget. You can start with a free coverage review at any of our 14 Houston-area offices — same-day appointments are available.

Harris County: Why Houston Flood Risk Is Not What Most Homeowners Think

Harris County has sustained more flood damage than any other county in the United States. This is not a ranking based on one bad storm. It is a cumulative record built over decades of major flood events — Allison in 2001, Ike in 2008, the Tax Day Flood in 2016, Harvey in 2017, and a long series of significant flooding events before and between those storms.

The reasons are structural and geographic:

Elevation: Large portions of Harris County sit at or near sea level, giving floodwater little gradient to drain

Soil: The region's clay-heavy soil has extremely low permeability — rainfall sits on the surface rather than soaking in

Bayou network: Houston's bayou system, while extensive, was not engineered to handle the rainfall volumes that modern storm systems produce

Development: Decades of impervious surface expansion — roads, parking lots, rooftops — has reduced the land's natural ability to absorb runoff, accelerating flooding in downstream neighborhoods

Storm track: The Gulf of Mexico is warm, and warm Gulf water intensifies tropical systems rapidly. Storms that reach the Texas coast often arrive stronger and wetter than forecast

FEMA's flood maps, which designate "Special Flood Hazard Areas," are based on historical data and are updated infrequently. Harvey demonstrated conclusively that a majority of flooded homes were outside mapped flood hazard zones. In practical terms: being outside the 100-year flood plain in Harris County does not mean your flood risk is low. It means you are in a county that floods — and that your particular neighborhood has not flooded as recently or as deeply as mapped high-risk zones have.

Renters are not exempt from this risk. If you rent your home and a flood event damages or destroys the structure, your landlord's policy covers the building — not your belongings. A renters insurance quote with a conversation about flood options for personal property is worth having before June 1 passes. If you rent, it helps to know whether renters insurance is worth it, the key considerations before you choose your limits, and — if you have a young adult in their first apartment — why kids moving out need their own renters policy.

The 30-Day Waiting Period and Hurricane Season: The Math Every Houston Homeowner Needs to Do

Hurricane season runs June 1 through November 30. The Gulf of Mexico typically becomes its most active between late August and mid-October, but named storms have struck Texas in June and July. If you have not gotten your home and vehicles storm-ready yet, our hurricane season preparedness guide is a practical place to start.

The NFIP's 30-day waiting period means that coverage purchased today — in late May or early June — would activate approximately 30 days from the purchase date. Coverage purchased at the beginning of June would be active by early July, before the Gulf reaches peak season temperatures.

The waiting period is not waived for any named storm already being tracked. Once the National Hurricane Center issues advisories on a system targeting the Gulf or Texas coastline, it is too late. Carriers and FEMA are explicit: if a storm is being tracked and you attempt to purchase flood insurance, the waiting period still applies. You will not be covered for damage from that storm.

This is why the timing of this article matters. We are publishing this in early June 2026 — before the major storm season peak, before any named storms are being tracked toward Texas, and before it is too late. The homeowners who read this, act this week, and purchase flood insurance will have active coverage by early July. The homeowners who bookmark this article and wait until a storm forms will not.

The step is not complicated:

Call or walk into any of our 14 AZ Insurance offices

Tell us you want to review your homeowners policy and look at flood options

We will compare NFIP and private flood options for your property

You can have a policy bound the same day

No storm on the radar. No waiting for a news alert. No hoping your neighborhood stays dry. Just coverage.

What Flood Insurance Does Not Cover That Homeowners Forget

Even homeowners who do purchase flood insurance sometimes discover gaps after a claim. It is worth understanding what flood policies — both NFIP and many private options — typically do not cover, so you can plan accordingly:

Additional living expenses: NFIP does not pay for your hotel, temporary rental, or meals while your home is uninhabitable. Some private flood policies do; NFIP does not. This can represent tens of thousands of dollars out-of-pocket during a multi-month repair process

Detached structures: Most NFIP policies do not cover detached garages, sheds, fences, or pools under standard terms

Landscaping and hardscaping: Trees, shrubs, patios, driveways, and other outdoor improvements are generally not covered

Basement contents: NFIP limits coverage for items stored in basements, even with a contents policy. Furniture, electronics, and personal property kept below grade may have limited or no coverage

Currency, precious metals, and important papers: NFIP excludes these categories

Vehicles: Cars, trucks, and motorcycles damaged by flooding are covered under the comprehensive portion of your auto insurance policy, not under your flood insurance policy (if you are unsure how that side of your coverage works, here is the main purpose of auto insurance)

High-value items above policy limits: Jewelry, art, and collections above certain limits require separate scheduled coverage

Understanding these gaps before a loss — not after — is the point of a coverage review. Our team will walk through your full exposure so you are not surprised by what a policy does and does not cover. The same goes for the rest of your homeowners policy: our guides on staying out of the doghouse with home insurance, protecting your home through the holidays, and whether prefabricated homes require insurance cover the year-round basics.

Frequently Asked Questions

Q: My home is not in a flood zone. Do I still need flood insurance in Houston?

Yes. The majority of homes flooded during Harvey were outside FEMA-designated Special Flood Hazard Areas. Harris County's hydrology means that even low-risk zones can flood during major storm events. Flood zone designation determines whether your lender requires you to purchase flood insurance — it does not determine whether your home can flood.

Q: How much does flood insurance cost in Houston?

Flood insurance premiums vary based on your property's elevation, construction type, flood zone designation, coverage amounts, and whether you choose NFIP or a private carrier. NFIP rates in low-to-moderate risk zones are often lower than many homeowners expect. A coverage review with our team will give you actual numbers for your specific address. Request a homeowners insurance quote to get started.

Q: How long does it take for flood insurance to activate after I buy it?

NFIP policies have a standard 30-day waiting period before coverage activates. Some private flood insurers offer shorter waiting periods — in some cases as short as 10 to 14 days. If a storm is already being tracked, neither option will protect you from that specific storm. Act before the forecast changes.

Q: Can I buy flood insurance directly from the government?

You purchase NFIP policies through licensed insurance agents — not directly from FEMA. Our agents at AZ Insurance are authorized to write NFIP policies and can compare NFIP against private flood options to find the best fit for your home and budget.

Q: My lender is requiring me to buy flood insurance. What are my options?

If you have a federally-backed mortgage (FHA, VA, Fannie Mae, Freddie Mac) and your home is in a Special Flood Hazard Area, your lender is required by law to ensure you carry flood insurance. You can typically satisfy this requirement with either an NFIP policy or a qualifying private flood policy. We can help you navigate the lender requirements and find coverage that satisfies the mandate and fits your budget.

Q: Does homeowners insurance cover water damage from a hurricane?

It depends on the source. Wind-driven rain that penetrates a damaged roof during a hurricane may be covered under your homeowners policy — though wind and hail claims are usually subject to a separate percentage-based deductible that catches many homeowners off guard (we break this down in Texas Storm Deductible Explained). Floodwater that enters your home due to storm surge, rising bayous, or sheet flooding from rainfall is not covered — that requires a separate flood insurance policy. The distinction matters enormously because most of the damage from major Texas hurricanes comes from flooding, not from the wind itself.

Why AZ Insurance Stands Apart

AZ Insurance has been serving Houston homeowners since 2003. We have 14 offices across the Houston area, we serve families in English and Spanish, and when you walk in for a coverage review, we are comparing options from 8 carriers — not selling you the one product we happen to carry. On flood coverage, that means we can show you NFIP side-by-side with private flood alternatives and tell you honestly which one fits your home, your risk profile, and your budget. We have been through Harvey. We have seen what a gap in flood coverage costs a family. We do not want that conversation to happen to you after the water rises.

Request a free coverage review at your nearest AZ Insurance office today — same-day appointments are available at all 14 Houston-area locations.

Related Articles

Latest Blogs

Are You Underinsured? How Much Dwelling Coverage Your Houston Home Needs

What Is Business Personal Property Insurance Coverage and Why Does It Matter?

Your Roof and Texas Home Insurance: Age, Depreciation, and Nonrenewal

Sole Proprietor Business Insurance: Common Risks and How to Protect Yourself

Actual Cash Value vs Replacement Cost: What Every Texas Homeowner Needs to Know Before the Next Storm

Does Your Health Insurance Work Abroad? A Houston Guide

Let A-Z Auto Insurance Help You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto Insurance Help

You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto

Insurance Help You

Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Let A-Z Auto Insurance Help

You Find Affordable Coverage

Connect with our experienced team today & get reliable, affordable insurance designed around your needs.

Contact Us!

Latest New & Blogs

Latest New & Blogs

Related Blog Posts

Related Blog Posts

Your Roof and Texas Home Insurance: Age, Depreciation, and Nonrenewal

Roof age is one of the biggest factors Texas carriers use to set premiums and decide coverage. Here is what Houston homeowners need to know before their next renewal.

Your Roof and Texas Home Insurance: Age, Depreciation, and Nonrenewal

Roof age is one of the biggest factors Texas carriers use to set premiums and decide coverage. Here is what Houston homeowners need to know before their next renewal.

Your Roof and Texas Home Insurance: Age, Depreciation, and Nonrenewal

Roof age is one of the biggest factors Texas carriers use to set premiums and decide coverage. Here is what Houston homeowners need to know before their next renewal.

Sole Proprietor Business Insurance: Common Risks and How to Protect Yourself

What is the sole proprietor for business insurance, and do you need it? Learn the biggest risks, coverage types, & how to protect your Texas sole proprietorship.

Sole Proprietor Business Insurance: Common Risks and How to Protect Yourself

What is the sole proprietor for business insurance, and do you need it? Learn the biggest risks, coverage types, & how to protect your Texas sole proprietorship.

Sole Proprietor Business Insurance: Common Risks and How to Protect Yourself

What is the sole proprietor for business insurance, and do you need it? Learn the biggest risks, coverage types, & how to protect your Texas sole proprietorship.

Actual Cash Value vs Replacement Cost: What Every Texas Homeowner Needs to Know Before the Next Storm

ACV pays the depreciated value of your roof or belongings. Replacement cost pays to rebuild new. Texas storm numbers show the gap can be thousands.

Actual Cash Value vs Replacement Cost: What Every Texas Homeowner Needs to Know Before the Next Storm

ACV pays the depreciated value of your roof or belongings. Replacement cost pays to rebuild new. Texas storm numbers show the gap can be thousands.

Actual Cash Value vs Replacement Cost: What Every Texas Homeowner Needs to Know Before the Next Storm

ACV pays the depreciated value of your roof or belongings. Replacement cost pays to rebuild new. Texas storm numbers show the gap can be thousands.

Your Roof and Texas Home Insurance: Age, Depreciation, and Nonrenewal

Roof age is one of the biggest factors Texas carriers use to set premiums and decide coverage. Here is what Houston homeowners need to know before their next renewal.

Sole Proprietor Business Insurance: Common Risks and How to Protect Yourself

What is the sole proprietor for business insurance, and do you need it? Learn the biggest risks, coverage types, & how to protect your Texas sole proprietorship.